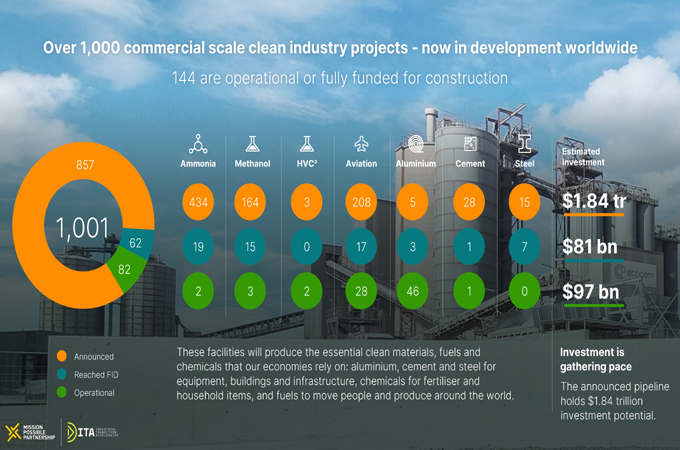

The Industrial Transition Accelerator (ITA) and Mission Possible Partnership (MPP) announced that clean industry is entering a new phase of momentum, with 1,001 commercial-scale projects now recorded across all stages of development.

This marks strong growth across multiple sectors and regions despite ongoing geopolitical headwinds.

New data published in MPP’s Global Project Tracker, supported by the ITA, reveals 144 commercial-scale projects worldwide have now reached final investment decision (FID).

Of these, 82 are operational and 62 have secured funding, spanning the most energy-intensive sectors: aluminium, cement, chemicals, fuels for aviation and shipping, and steel.

A global opportunity wide open for the taking

The Global Project Tracker data identifies clean industrial plants in development or operational across 70 countries, representing nearly $2 trillion in remaining investment potential.

The ‘new industrial sunbelt’, a region rich in renewable energy resources spanning Latin America, Australia, Africa and Asia, claims the largest share of this opportunity, with India now home to the world’s third-largest clean industry pipeline and Brazil not far behind.

As clean industry continues to gain momentum, the coming months are set to be even more transformational, with 70 projects identified beyond China as poised for financing and representing a combined value of $140 billion.

More than a third of these projects are located in emerging economies from Brazil to Namibia, where realising this opportunity could rapidly unlock significant benefits for sustainable economic growth, supply chain resilience and job creation.

The Global Project Tracker data illustrates the massive investment potential for clean industry to grow economies, but also notes that this potential is dependent on stronger demand-side policy.

The ITA has worked with partners across the value chain to test new approaches, support project developers and improve investment conditions, helping more projects move toward their goal of FID.

In Brazil, Acelen Renewables are harnessing the potential of Brazil’s existing deforested and degraded land to build the first ‘seed to fuel’ large-scale project turning macaúba into jet fuel for global markets, while providing new opportunities to local communities.

Elsewhere, Hydro Alunorte, is the world’s largest alumina refinery outside of China, and is implementing a multi-phase strategy of electrification and biomass integration while maintaining its market competitiveness.

In India, with its healthy pipeline of 47 projects in development, the benefits of energy security and resilience to external shocks are matched by the job creation and inward investment opportunities.

China is racing ahead

China is moving rapidly to claim an early strategic

advantage, with 12 projects reaching FID in the past year and 54 confirmed overall,

surpassing any other region.

This speed is driven by an unprecedented renewable

energy build-out and proactive industrial policy.

Most of these projects span the methanol, ammonia

and aviation sectors to meet domestic and international clean fuel demand.

However,

current supplies will only meet a small fraction of what will be needed for global

trade and travel.

In south-west China, the first production line

of the China Hongqiao Group’s aluminium facility began operating in July of this

year.

Powered

by 4 GW of solar energy, it is expected to match the total aluminium output of North

American by 2026.

Meanwhile, the world’s first commercial-scale green ammonia plant became operational this summer at Envision Energy’s Green Hydrogen Park in Chifeng, China.

Clear routes to stronger, cleaner growth now

visible

Clean fuel markets are scaling fast. In aviation, the EU’s sustainable aviation fuel mandate came into force this year, while emerging national standards across Asia and the UK are expanding market demand.

In shipping, the International Maritime Organisation’s (IMO) target of 5 per cent clean fuel uptake by 2030 has spurred a wave of new ammonia and methanol projects from Singapore to Brazil, projects expected to accelerate once the IMO finalises its net-zero framework.

Progress in the ammonia and methanol industries

are especially significant, as both are expected to drive down the cost of clean

hydrogen production.

As prices

fall, clean fertiliser could soon undercut conventional ‘grey’ production – a shift

with major implications for food and energy security in import-dependent countries

such as India and Brazil.

These same investments are also laying the groundwork

for a broader clean hydrogen economy that will underpin industrial competitiveness

worldwide.

However, while existing and anticipated policies are driving demand in fuels, it remains limited in other sectors.

In cement, deep decarbonisation remains challenging,

but affordable solutions such as calcined clay are already cutting emissions by

up to 70 per cent, and at lower cost than traditional technology.

Reducing clinker import dependence and lowering

construction costs strengthens economic resilience, allowing emerging markets to

build faster and cleaner.

Leading developers based in Europe and North Africa, including Ecocem, Vicat and CBI, report strong demand from the construction industry.

Faustine Delasalle, Mission Possible Partnership CEO and Executive Director of Industrial Transition Accelerator: “It’s taken nearly a decade to reach this point. With a record number of operational and under construction plants across all sectors, clean industry is no longer a vision for the future, it is a burgeoning opportunity we can speed up today. Building on the leadership of many companies around the world, governments and investors have a unique opportunity to turn today’s plans into plants, which together will make up tomorrow’s global clean industrial economy. Those who demonstrate strategic foresight and unwavering commitment to the clean industrial transition stand to reap its benefits.”

Policy action will determine who captures the

opportunity

The evidence is clear: there is profit potential

in clean industry, but the pace of financing depends on stronger demand-side policy.

Governments that create predictable demand signals for clean materials, chemicals, and fuels will unlock the next wave of projects and secure their industrial futures.

The ITA’s work on demand-side policy in Europe

highlights this opportunity: by creating lead markets for clean materials and fuels,

the EU could revive its flagging industries and boost its pipeline of projects,

which represents more than €100 billion ($117.6 billion) in investment potential.

Such measures would strengthen supply chain resilience and energy security while adding only marginally to the cost of consumer goods, far less than inflation caused by volatility from fossil fuel-intensive production.

Industrial Transition Accelerator leading collaboration

for change

Launched at COP28 in Dubai by the COP28 Presidency,

Bloomberg Philanthropies and United Nations Climate Change, the ITA was created

to accelerate the decarbonisation of heavy- emitting industry and transport and

drive investment into projects consistent with a Paris- aligned pathway.

The initiative brings together partners from government, industry, finance and civil society to tackle global challenges, and works directly with project developers across Brazil, UAE, Bahrain, Egypt, and as also announced today, India.

Enable investment to Build Clean Now

The Global Project Tracker shows that a clean industry transformation is now clearly underway, with a diverse pipeline ready for investment.

Through the Build Clean Now campaign, MPP, ITA and partners are working with governments, investors and industry to identify solutions to unlock the most advanced clean industrial projects and accelerate the pace at which they are financed and built, year-on-year – to build prosperity, resilience and opportunity across every region. -OGN/TradeArabia News Service

Send us your company’s news today and they could be featured on ABC’s Community News tommorow.